01 Aug 2018

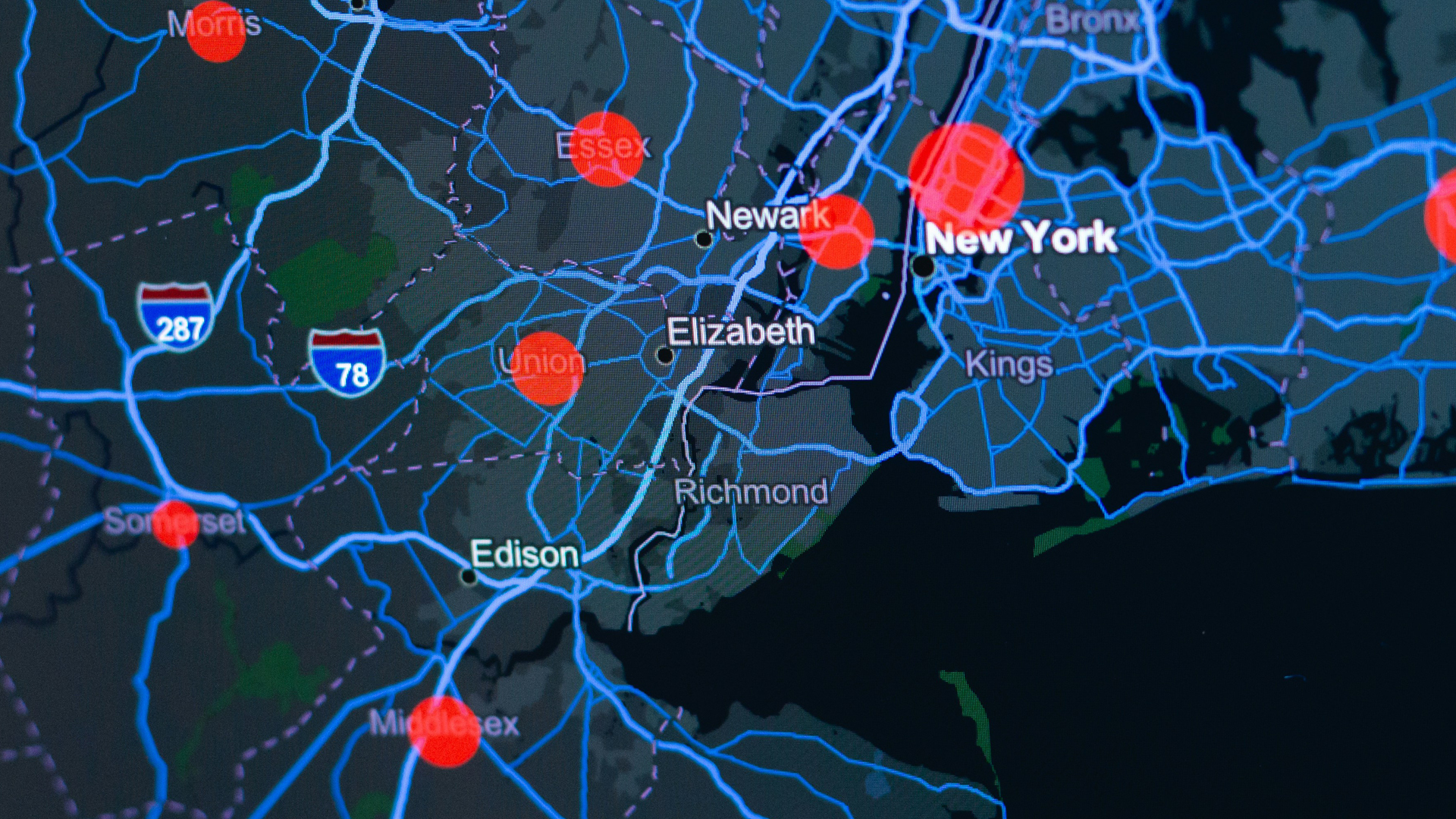

2018 will undoubtedly be the largest year ever for new self storage deliveries. Tracking all this activity as part of acquisition, disposition or new development has become crucial for any self storage analyst. In many cases, knowing a new competitor will be opening soon is enough to deter further investment in that market.

However, as we progress through the fourth year of the self storage development cycle we find it prudent to not only analyze prospective competition but recent openings. As lease up times extend to 2–3 years (depending on the region) we find that facilities already delivered during this cycle will continue to have an impact on rental rates.

1,442 Facilities have been delivered since January 1, 2016. Square footage growth across the country in 2016 and 2017 was 1.3% and 2.8% respectively. Through Q1 of 2018 there has already been 243 facilities delivered or 0.9% increase in supply.

The chart below illustrates that regions with greater supply growth over the last two years are seeing rental rates soften the by the largest magnitude. Interestingly, regions with less than 1% increase in supply per annum see roughly flat to increasing rates which would suggest an appropriate level of growth for orderly absorption.

As we outline below, the impact of all these deliveries will likely persist for a couple years. Monitoring absorption rates will be key to determining when the impact to rental rates subsides.